In July 2026, The Goldman Sachs Group (GS) is trading at the intersection of record fundamentals and a stretched valuation. On July 14, the firm posted the strongest quarter in its history: net revenues of $20.34 billion and diluted EPS of $20.98, beating a consensus near $14.46 by roughly 45%. The stock jumped more than 8% on the print to trade near $1,140, extending a year-to-date gain that ran above 20% before the release. Investors remain divided. Bulls point to a $1 trillion first-half M&A advisory pipeline, the fastest pace ever recorded by an investment bank, while skeptics highlight a Hold consensus, a fresh Oppenheimer downgrade to Underperform on valuation, and a consensus target that sits below the current price.

The Q2 report was not a cost-cutting story. Revenue rose about 39% year over year while net margin expanded to roughly 32.6%, and annualized return on equity reached 23.5%. Goldman is now the clearest listed proxy for two simultaneous capital markets waves: the AI investment cycle and the reopening of the blockbuster IPO window. This guide breaks down the GS stock price prediction for 2026 using data from the firm's own Q2 filings, Wells Fargo, Bank of America, Evercore ISI, Morgan Stanley, and Oppenheimer.

You will also discover how to gain exposure to Goldman Sachs (GS) stock futures through BingX TradFi.

Top 5 Things for Goldman Sachs Investors to Know in July, 2026

- Q2 EPS of $20.98 nearly doubled from $10.91: Net revenues reached $20.34 billion against $14.58 billion a year ago, with net earnings of $6.63 billion, beating a consensus near $14.46 by roughly 45%.

- M&A advisory volume crossed $1 trillion in the first half: Goldman captured roughly 42% market share at the fastest pace ever recorded by an investment bank, and its EMEA advised deals hit a 19-year high.

- Investment banking revenue rose about 55% to $3.4 billion: The line houses fees from the SpaceX IPO, a $25 billion SpaceX bond sale, and a co-lead role on Alphabet's $85 billion equity raise.

- Oppenheimer downgraded GS to Underperform on June 30: Chris Kotowski cut the rating on valuation grounds while raising his estimates, and the broader consensus target near $936 sits well below the post-earnings price.

- The quarterly dividend climbed roughly 11% to $5.00: The increase is supported by 23.5% quarterly ROE and book value per share of $367.67, up 2.8% across the first half.

What Is Goldman Sachs (GS)?

The Goldman Sachs Group, Inc. is a leading global financial institution that provides a wide range of financial services to a substantial and diversified client base. Following its pivot away from Main Street consumer banking, the firm is now a streamlined Wall Street pure-play built around fee generation and market-making.

Its competitive advantage lies in its top global ranking in completed M&A and equity underwriting. The firm operates through three primary segments: Global Banking & Markets, Asset & Wealth Management, and Platform Solutions. Under CEO David Solomon, the strategy focuses on high-ROE activities, leveraging a fortress balance sheet and roughly 295 million shares outstanding to capture fee-rich institutional mandates. Global Banking & Markets alone generated $15.52 billion in Q2 net revenues, up 53% from the second quarter of 2025.

Goldman Sachs' stock performance in 2025 | Source: Yahoo Finance

Goldman Sachs (GS) Q2 2026 Earnings: What Drove Record Revenue and EPS Growth

- Equity underwriting revenue rose about 130%: Debt underwriting climbed roughly 70% year over year, both ahead of estimates, as the IPO and issuance window reopened.

- AI investment is pushing more companies to raise capital: Management pointed to a favorable environment for strategic M&A and AI-related capital spending as a direct driver of the quarter.

- New retirement plan mandates added roughly $70 billion: Wins including Verizon and Lockheed Martin support the goal of $750 billion in alternatives AUM by 2030 and deepen recurring fee income.

- Goldman is a favorite to lead OpenAI's pending IPO: The firm shares that position with Morgan Stanley, and the mandate would lift second-half underwriting fees materially if it lands.

Goldman Sachs (GS) Q2 2026 Financial Health: Record Revenue, EPS and ROE

Goldman entered the second half of 2026 with the strongest financial profile in its history. First-half net revenues reached $37.57 billion and net earnings $12.26 billion, producing first-half EPS of $38.51 against $25.07 a year earlier. Annualized ROE was 23.5% for the quarter and 21.7% for the half, while book value per common share rose 2.8% in the first six months to $367.67.

The tension sits in the multiple rather than the operations. The trailing P/E near 20.8x runs roughly 43% above the five-year median of about 14.5x, and at least one intrinsic value model places fair value far below the market price. The dividend yields around 1.75% after the increase to $5.00 quarterly. The question for the second half is whether the deal pipeline sustains the run rate that the current multiple already assumes.

Goldman Sachs (GS) 2026 Investment Outlook: Alpha vs. Insider Selling

Goldman Sachs' stock forecast for 2026 by Wall Street analysts

The remainder of 2026 for GS is a tug-of-war between record earnings power and a valuation that several high-accuracy analysts already view as full.

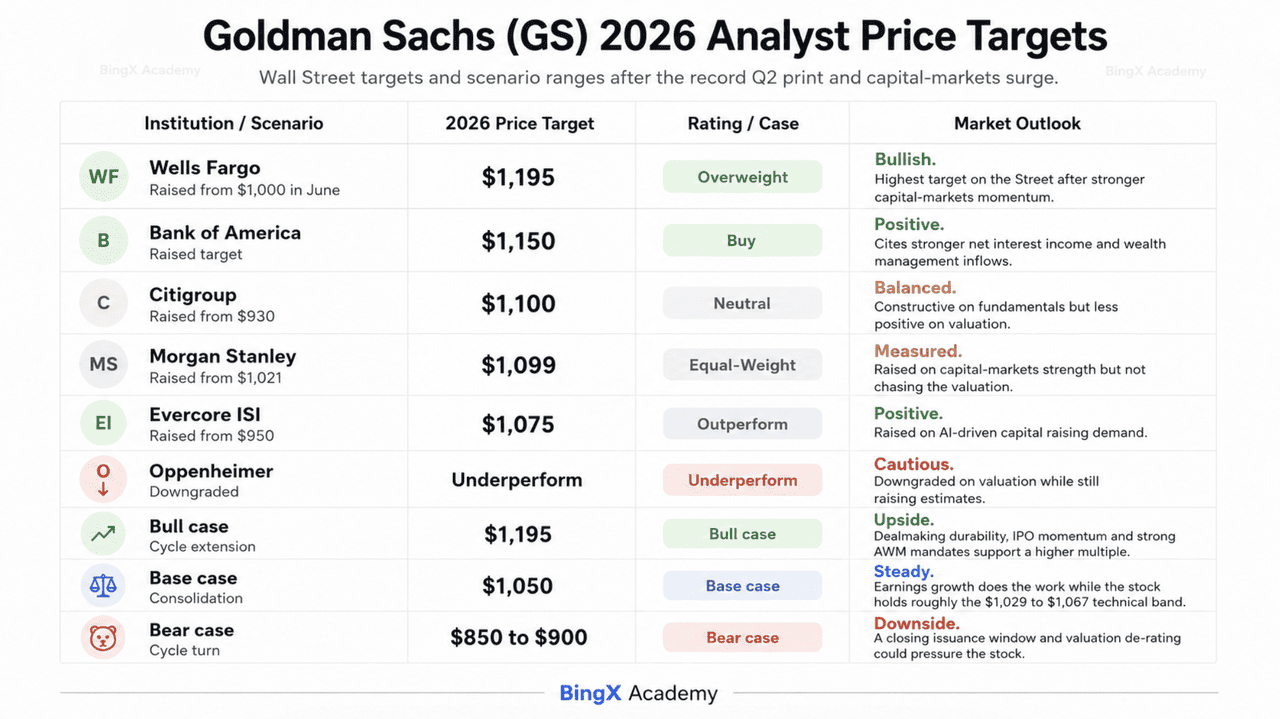

The Bull Case: Goldman Sachs' $1,195 Cycle Extension

The bull narrative rests on the durability of the dealmaking cycle rather than a single catalyst. Goldman advised on more than $1 trillion of announced M&A in the first half with roughly 42% market share and 71% year-over-year growth in deal value, and it ranked first in global M&A fees for the period according to LSEG data. If that pipeline converts through the back half, the Q2 revenue run rate is a floor rather than a peak, and Wells Fargo's Mike Mayo has anchored the high end of the Street at $1,195.

Practically, this scenario requires the underwriting window to stay open. A lead role on the OpenAI IPO would add substantial fees to third and fourth quarter consensus, layered on top of the SpaceX and Alphabet mandates already booked. Sustained ROE above 20% alongside $70 billion in new AWM mandates would support the argument that recurring fee income has structurally reduced Goldman's dependence on trading volatility, justifying a permanently higher multiple rather than a cyclical one.

The Base Case: GS Stock's $1,050 Consolidation

In the base case, Goldman digests the record quarter and consolidates. The stock jumped more than 8% on the print, closing much of the gap to the highest targets on the Street, and Bank of America's $1,150 and Evercore ISI's $1,075 now sit close to or below the market. That leaves limited room for multiple expansion even if earnings continue to beat.

For investors, this scenario is defined by earnings growth doing the work while the multiple stays flat or compresses modestly. The consensus rating remains Hold across roughly 14 analysts, and the aggregate target near $936 reflects targets set before the Q2 beat that have not yet fully caught up. Steady trading revenue, the raised $5.00 dividend, and expanding AWM fee income support a price that holds the $1,029 to $1,067 technical band while the Street revises models upward.

The Bear Case: Goldman Sachs Stock Toward $850 on a Cycle Turn

The bear case does not require Goldman to execute poorly. It requires the cycle to turn. Oppenheimer's June 30 downgrade to Underperform came alongside raised Q2 estimates, which is the point: the firm argued that the cycle may run another 12 to 18 months but that the risk-reward no longer favors waiting for warning signs. A sum-of-parts valuation cited in that framework pegs fair value closer to $732.

The trigger would be a closing of the issuance window. Higher bond yields, a Federal Reserve pivot back toward restriction, or renewed AI-related caution prompting OpenAI and other candidates to delay IPOs would remove the underwriting fees that drove the 130% equity underwriting surge. Advisory revenue already came in slightly below consensus in Q2 despite the record headline. If the M&A backlog stops converting while the stock carries a 20.8x trailing multiple against a 14.5x five-year median, a rapid de-rating toward the $850 to $900 range becomes the path of least resistance.

GS Stock Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Wells Fargo |

$1,195 |

Overweight: Highest target on the Street, raised from $1,000 in June. |

|

Bank of America |

$1,150 |

Buy: Cites stronger net interest income and wealth management inflows. |

|

Citigroup |

$1,100 |

Neutral: Raised from $930, constructive on fundamentals but not valuation. |

|

Morgan Stanley |

$1,099 |

Equal-Weight: Raised from $1,021 on capital markets strength. |

|

Evercore ISI |

$1,075 |

Outperform: Raised from $950 on AI-driven capital raising demand. |

|

Oppenheimer |

Underperform |

Underperform: Downgraded on valuation while raising estimates. |

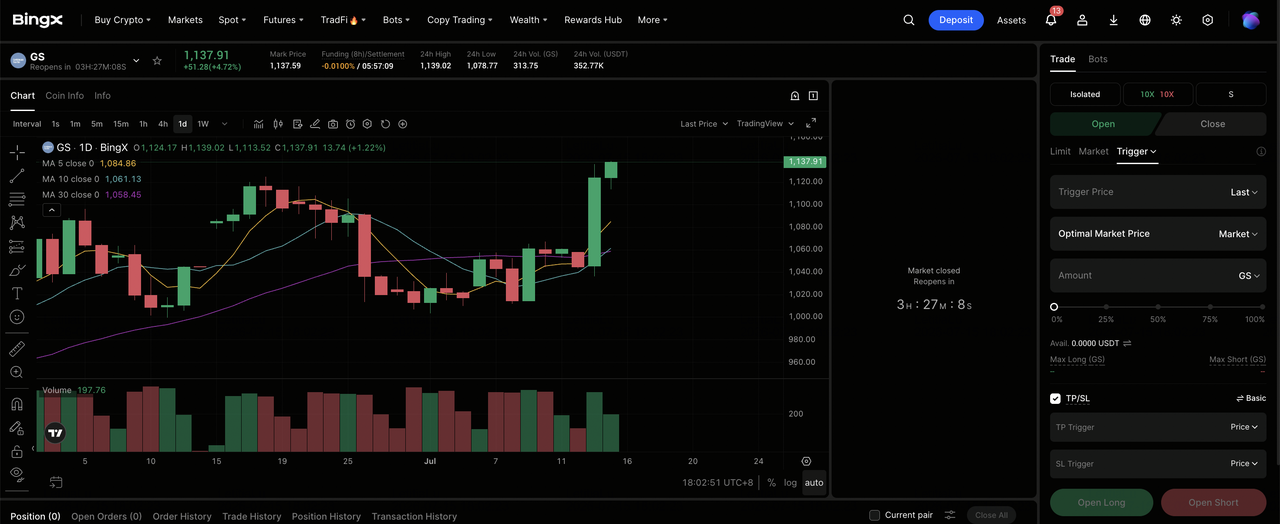

How to Trade Goldman Sachs (GS) Stock on BingX

Maximize your trading potential by using BingX AI tools to navigate Goldman's post-earnings volatility.

Long or Short Goldman Sachs Stock Futures on BingX TradFi

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select The Goldman Sachs Group (GS). Search for and select the GS-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect the dealmaking cycle to extend, the OpenAI IPO mandate to land, and Asset & Wealth Management inflows to keep compounding. Select Open Short if you expect the issuance window to close, advisory conversion to slow, or a valuation de-rating toward the consensus target that still sits below the market price.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because GS moved more than 8% in a single session on the Q2 print, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. GS can react quickly to quarterly earnings, M&A pipeline data, IPO calendar shifts, analyst rating changes, and Federal Reserve rate commentary.

Top 5 Risks to Watch for Goldman Sachs Investors in 2026

To navigate the second half of 2026, investors must balance Goldman's record operating performance against these five critical macro and operational headwinds.

- The trailing P/E of 20.8x runs 43% above its five-year median: With the aggregate analyst target near $936 sitting below the post-earnings price, new entrants have no margin of safety at current levels.

- Insiders sold roughly $35.6 million of stock with no buying: The pattern spanned the prior three months, and one-sided insider activity has historically tended to accompany local valuation peaks.

- The underwriting surge depends on an issuance window staying open: An OpenAI IPO delay or a broader pullback in AI-linked issuance would remove the fees that produced the quarter's headline growth.

- Global Banking & Markets supplied $15.52 billion of $20.34 billion in Q2 revenue: That concentration explains the record print and the speed at which a cycle turn would hit earnings.

- Higher bond yields would pressure deal volumes and credit at once: A Federal Reserve shift back toward restriction attacks both inputs the current multiple assumes remain benign.

Final Thoughts: Should You Invest in Goldman Sachs (GS) in 2026?

Goldman Sachs after the July 14 report is a story of an operationally flawless franchise trading at a cyclical peak. Record revenue, record EPS, 23.5% ROE, and the largest first-half advisory volume in Wall Street history are not in dispute. What is in dispute is what an investor should pay for a business whose earnings power is this cycle-dependent.

The bull case is that recurring fee income from Asset & Wealth Management has structurally lowered Goldman's cyclicality, justifying a higher multiple. The bear case, articulated by one of the Street's most accurate analysts while simultaneously raising estimates, is that the cycle has 12 to 18 months left and the stock already prices in the good news. Investors who believe the AI and IPO waves have further to run may find the franchise remains the highest-quality expression of that view. More conservative traders might wait for a retest of the $1,014 to $1,029 area before initiating a long-term position.

Risk Reminder: Trading and investing in equities like GS involves a high risk of capital loss. Goldman’s heavy reliance on market volatility and regulatory shifts introduces significant price swings. Conduct independent research before allocating capital.

Related Reading

- GE Aerospace (GE) Price Prediction 2026: Can the $190B Backlog Defy Valuation Fears?

- Ferrari N.V. (RACE) Stock Outlook for 2026: Can An Iconic Brand and EVs Drive RACE Stock to $550+?

- Mastercard (MA) Stock Price Forecast for 2026: Fintech Giant or Regulatory Target?

- Circle (CRCL) Stock Outlook for 2026: Can USDC Growth and Dominance Drive CRCL Stock to $250+?

- JPMorgan Chase (JPM) Price Prediction 2026: Fortress Defense or AI-Driven Alpha at $341?

- Morgan Stanley (MS) Price Prediction 2026: Investment Bank Resurgence or $170 Correction?