In mid-June 2026, Corning Incorporated (NYSE: GLW) finds itself positioned at a dramatic crossroads between unprecedented structural AI data center demand and looming cyclical macro headwinds. Booming on a spectacular vertical rally that has driven the equity up 97.6% year-to-date and over 256% over the past year, the New York-headquartered hardware specialist is currently trading near $187.88.

While the stock spent the early part of the decade viewed as a mature, low-beta industrial legacy play, back-to-back operational breakthroughs have completely supercharged its multi-year revenue outlook. Investors are aggressively weighing an exceptionally strong first-quarter earnings report and updated Springboard guidance against an overvaluation narrative that has pushed trailing multiples to historic highs.

As the global technology ecosystem transitions toward specialized, high-density generative AI and agentic frameworks, the absolute necessity for massive fiber-optic connectivity has transformed Corning into a primary infrastructure bottleneck. However, a sharp cyclical slowdown in traditional consumer electronics and elevated insider selling have created a persistent valuation debate.

This guide breaks down the Corning Incorporated stock forecast and price prediction for the remainder of 2026, utilizing data from S&P Global Market Intelligence, UBS Group, Mizuho, Citi, LSEG consensus estimates, and official regulatory disclosures.

You will also discover how to trade Corning Incorporated (GLW) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Corning (GLW) Traders to Know in 2026

As Corning navigates a high-stakes environment of exponential optical scaling and intensive valuation scrutiny, traders must closely monitor these five market-moving factors:

- The Billion-Dollar Amazon AI Megadeal: Announced on June 8, 2026, Amazon has entered a multi-billion-dollar multi-year agreement to purchase Corning's high-density optical fiber, cable, and connectivity solutions. This partnership is designed to power and link AWS’s rapidly expanding U.S. artificial intelligence data center clusters and will create 1,000 manufacturing jobs in North Carolina.

- The $3.2 Billion NVIDIA Alliance: In May 2026, NVIDIA committed up to $3.2 billion in capital to Corning. The deal includes building three new advanced manufacturing plants in North Carolina and Texas entirely devoted to the chipmaker, expanding Corning's optical connectivity manufacturing capacity by 10-times to support next-generation architecture.

- Stretched Valuation Multiples: Trading at a trailing price-to-earnings (P/E) ratio of 85.21x and a forward expected P/E of approximately 48x to 56x, Corning is priced at a severe expansion from its three-year historical average P/E of 21x. Intrinsic models, including Simply Wall St's 2-Stage Discounted Cash Flow (DCF), peg its fair value at $155.53, suggesting the stock is trading at a premium.

- The Cyclical Smartphone Drag: While AI infrastructure booms, Corning's traditional Glass Innovations segment, accounting for 32% of total revenue, stalled at just 1% year-over-year growth in Q1 2026. Industry forecasts project global smartphone shipments will contract between 7% and 15% in 2026 due to component shortages, directly pressuring high-margin Gorilla Glass volumes.

- The Springboard Plan Upgrade: At its May 2026 investor day, management upgraded its "Springboard Plan," targeting an annualized sales run rate of $20 billion by the end of 2026, representing a 15% CAGR from Q4 2023. Looking further ahead, management outlined ultra-bullish scenarios reaching $30 billion by 2028 and up to $40 billion by 2030, driven by its new Photonics Market-Access Platform (MAP).

What Is Corning Incorporated (GLW)?

Corning Incorporated (GLW) is a global leader in materials science, specialized glass, ceramics, and optical physics. Founded in 1851, the company has historically pioneered major technological shifts, from manufacturing the glass envelopes for Thomas Edison's light bulbs to inventing low-loss optical fiber in 1970 and developing the ultra-durable Gorilla Glass used by Apple and other major smartphone OEMs.

As of mid-2026, Corning represents a critical engineering gateway between cloud hyperscalers building out massive generative AI models and the physical hardware layer. Because AI clusters require thousands of graphic processors to communicate almost instantaneously, traditional copper wiring is inadequate due to latency and power constraints. Corning’s high-bandwidth optical cables, connectors, and customized photonics architectures solve this hardware bottleneck, making the company an indispensable enabler of AI data centers.

Corning's Performance in Early 2026: The Post-Earnings Repricing

Corning (GLW) stock performance YTD as of June 2026 | Source: Google Finance

Corning kicked off its 2026 fiscal year by reporting a blowout first-quarter financial release on April 28. Core sales surged 18% year-over-year to reach $4.35 billion, comfortably beating Wall Street consensus estimates. The core insight hiding beneath this headline beat is how completely the AI-driven acceleration is offsetting the modest growth seen in traditional segments.

|

Q1 2026 Metric |

Reported Value |

Year-over-Year (YoY) Change |

|

Core Sales |

$4.35 Billion |

0.18 |

|

Core EPS |

$0.70 |

0.3 |

|

Optical Communications Sales |

$1.80 Billion |

0.36 |

|

Solar Infrastructure Sales |

N/A |

0.8 |

|

Core Operating Margin |

20.20% |

+220 bps |

Crucially, structural demand for high-density AI data center architectures allowed Corning to secure expansion deals alongside its massive, legacy $6 billion supply agreement with Meta Platforms. This combined secular strength expanded core operating margins by 220 basis points to 20.2%. Management subsequently guided Q2 2026 sales to approximately $4.6 billion (+14% YoY) and core EPS to a range of $0.73 to $0.77, sparking a dramatic institutional upward repricing of the equity.

Corning's 2026 Trading Strategy: Navigating Volatility Multiples

- The $180 Support Floor: Technical analysts point to the $180 to $185 structural window, reinforced by recent multi-billion dollar project announcements, as a critical near-term support floor. As long as GLW respects this level on weekly candle closes, the parabolic momentum established during the first half of 2026 remains structurally intact.

- Evaluating Stretched Multiples vs. Cash Flow: Trading at an 85.21x trailing P/E, Corning looks heavily extended compared to the broader Electronic industry average of 32.91x. Short-sellers continue to flag a widening valuation gap, noting that investors are valuing a capital-intensive materials manufacturer at a premium typically reserved for asset-light software monopolies.

- The Insider Selling & Technical Pullback: Carrying a historic 52-week trading range of $49.81 to $211.79, GLW has experienced heightened volatility. Following a minor 6.6% monthly pullback from its June peaks, traders must monitor if elevated insider selling, exceeding $54 million in a recent quarter, signals institutional distribution or a short-term local top.

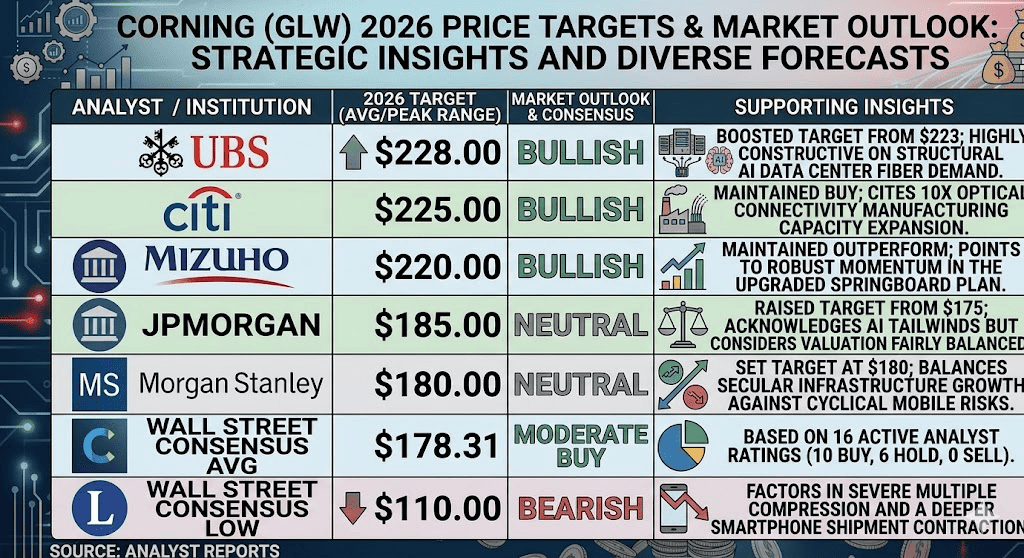

Corning 2026 Stock Forecast: $228 Street-High Peak vs. $110 Bear Case

Corning stock predictions for 2026 by Wall Street analysts

Evaluating Corning's forward trajectory requires balancing a high-confidence, multi-billion-dollar hyperscaler order book against the inescapable macro constraints of its capital-intensive manufacturing lines and consumer hardware exposures.

The Bull Case for Corning Stock: The $228+ Optical and Photonics Monopoly

The bullish thesis hinges on Corning completely locking down the global supply chain for AI data center optics. Championed by UBS Group's constructive target increase to $228 and Citi's boost to $225, this path assumes that the Amazon, NVIDIA, and Meta partnerships will sustain Optical segment growth above 35% annually.

In this scenario, Corning’s massive domestic factory buildouts seamlessly scale to capture the $700 billion in cumulative AI capital expenditures being deployed by tech giants this year. If the new Photonics Market-Access Platform completely dominates downstream Gen-AI architectures, and Q2 earnings in August deliver another massive beat, institutional capital will likely squeeze short-sellers, driving the asset past its $211.79 52-week high toward the premium $228 street-high target.

The Base Case: GLW's $168 – $190 Consolidation Plateau

The base case envisions a prolonged consolidation phase where the market systematically matches Corning's immense revenue growth against its cyclical headwinds. Under this framework, core earnings and revenue are forecast to grow by 26.2% and 16.8% per annum respectively over the next three years, outpacing the broader US market.

However, the stock faces a persistent cap on its current valuation multiple due to the pronounced smartphone market drag. If IDC data in July confirms a double-digit decline in global mobile shipments, the stagnation in Gorilla Glass volumes will offset a portion of the optical gains. For market participants, this setup favors a volatile, range-bound trading pattern between $168 and $190, roughly aligned with the Wall Street average price target of $178.31.

The Bear Case: The $110 Valuation and Cyclical Trap for GLW Stock

The bearish outlook focuses on multiple compression and structural margin erosion. If hyperscaler infrastructure spending normalizes below projected 2026 levels or if factory buildout costs in North America trigger margin-compressing overcapacity, the current premium multiple will contract rapidly.

Furthermore, if the consumer electronics recession worsens, or if technical maintenance shutdowns in the Solar wafer segment exceed guidance, a break below the structural $168 support line would invalidate the bullish trend. This would expose GLW to a steep mean-reversion selloff toward its historical averages, targeting the $110 Wall Street consensus low.

Corning (GLW) Price Predictions for 2026 by Wall Street Analysts

|

Institution |

2026 Price Target (Peak/Avg) |

Overall Market Outlook |

|

UBS Group |

$228.00 |

Bullish: Boosted target from $223; highly constructive on structural AI data center fiber demand. |

|

Citigroup |

$225.00 |

Bullish: Maintained Buy; cites 10x optical connectivity manufacturing capacity expansion. |

|

Mizuho |

$220.00 |

Bullish: Maintained Outperform; points to robust momentum in the upgraded Springboard plan. |

|

JPMorgan Chase |

$185.00 |

Neutral: Raised target from $175; acknowledges AI tailwinds but considers valuation fairly balanced. |

|

Morgan Stanley |

$180.00 |

Neutral: Set target at $180; balances secular infrastructure growth against cyclical mobile risks. |

|

Wall Street Consensus Avg |

$178.31 |

Moderate Buy: Based on 16 active analyst ratings (10 Buy, 6 Hold, 0 Sell). |

|

Wall Street Consensus Low |

$110.00 |

Bearish: Factors in severe multiple compression and a deeper smartphone shipment contraction. |

How to Trade Corning Incorporated (GLW) Stock Futures on BingX TradFi

GLW/USDT perpetual contract on BingX futures

As Corning navigates this high-stakes phase of exponential AI scaling and heavy headline volatility, tactical traders can seamlessly capitalize on its price action through the BingX platform:

- Access BingX TradFi: Navigate to the specialized TradFi section on your main BingX exchange dashboard.

- Select Corning (GLW): Search for and select the GLW-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe the multi-billion-dollar Amazon and NVIDIA data center contracts will drive the asset toward its $228 street-high target. Select Open Short to capitalize on trailing multiple overvaluation and potential technical pullbacks.

- Select Leverage and Margin Mode: Apply your preferred Isolated or Cross-Margin parameters alongside highly conservative leverage to optimize capital efficiency.

- Execute Strict Risk Protocols: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to lock in gains and protect your trading capital from abrupt gap moves during extended aftermarket hours.

Top 5 Risks to Consider Before Investing in GLW Stock

While Corning's position as a primary AI infrastructure enabler presents a compelling narrative, navigating this highly extended equity demands a rigorous assessment of its core risks:

- Severe Multiple Expansion Risk: Valued at 48x to 56x forward earnings, the market is pricing a high-capex industrial manufacturer like an asset-light software company, leaving zero margin for operational error.

- High Customer Concentration: Historically, a tiny cohort of buyers has dominated Corning's segments, e.g., three buyers accounting for 61% of automotive sales. Reliance on a few tech giant hyperscalers introduces structural vulnerability.

- Slowing Traditional Consumer Segments: A protracted double-digit global contraction in smartphone and computer monitor shipments will act as an anchor on the high-margin display glass portfolio.

- Elevated Insider Liquidation: Noted executive selling exceeding $54 million amid the 2026 rally can raise flags regarding inside leadership's short-term valuation expectations.

- Capital-Intensive Onshoring Costs: Building massive domestic fiber factories across North Carolina and Texas requires immense upfront capital expenditures, exposing margins to risk if deployment timelines stall.

Final Thoughts: Is Corning (GLW) Stock a Buy in 2026?

As of mid-June 2026, Corning Incorporated stands as one of the most fundamentally transformed and heavily debated plays within the AI infrastructure landscape. The company's ability to clear multi-billion-dollar order books with Amazon, Meta, and NVIDIA proves its absolute market relevance and confirms that its materials science moat is a vital component of the physical internet.

However, buying an industrial stock trading at over 85x trailing earnings requires strict caution. For short-term tactical traders, the equity provides an exceptional environment for daily volatility capture via BingX futures. Long-term investors, conversely, may find it prudent to wait for a deeper earnings-driven multiple contraction back toward the $155–$168 structural zone before allocating fresh, long-term capital.

Risk Reminder: Trading high-growth infrastructure equities involves significant capital risk due to elevated valuation multiples, capital-intensive manufacturing expansions, and cyclical consumer dependencies. Always enforce disciplined risk management, proper position sizing, and mandatory stop-losses.

Related Reading

- Meta (META) Stock Price Prediction 2026: Can AI Efficiency and Custom Silicon Drive META to $900?

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- AAOI Stock Prediction 2026: $260 Photonics Boom or Dilution Trap?

- Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure